AI and design: the future of customer experience

Read more

An integral part of service design involves sketching, simulating, or mapping user journeys. That means thinking through how someone experiences a service from start to finish, identifying friction and predictable mistakes, then designing the service so those mistakes are less likely (or less painful).

For businesses, the costs of failing to think about user journeys are perhaps easy to ignore. You may not stop to think about the time and money invested in resolving service failures, or where those investments might have been fruitfully spent instead. You may not consider the customers who, having also invested time and perhaps money of their own trying to resolve a problem, quietly drop off from your service.

The hidden costs of service failures accumulate - and even spiral - rapidly. The work of reducing them by applying the principles of service design unlocks serious value for your business and your customers.

These lessons are applicable to organisations across the board. But in this post I look at the example of banks and ATMs to illustrate them.

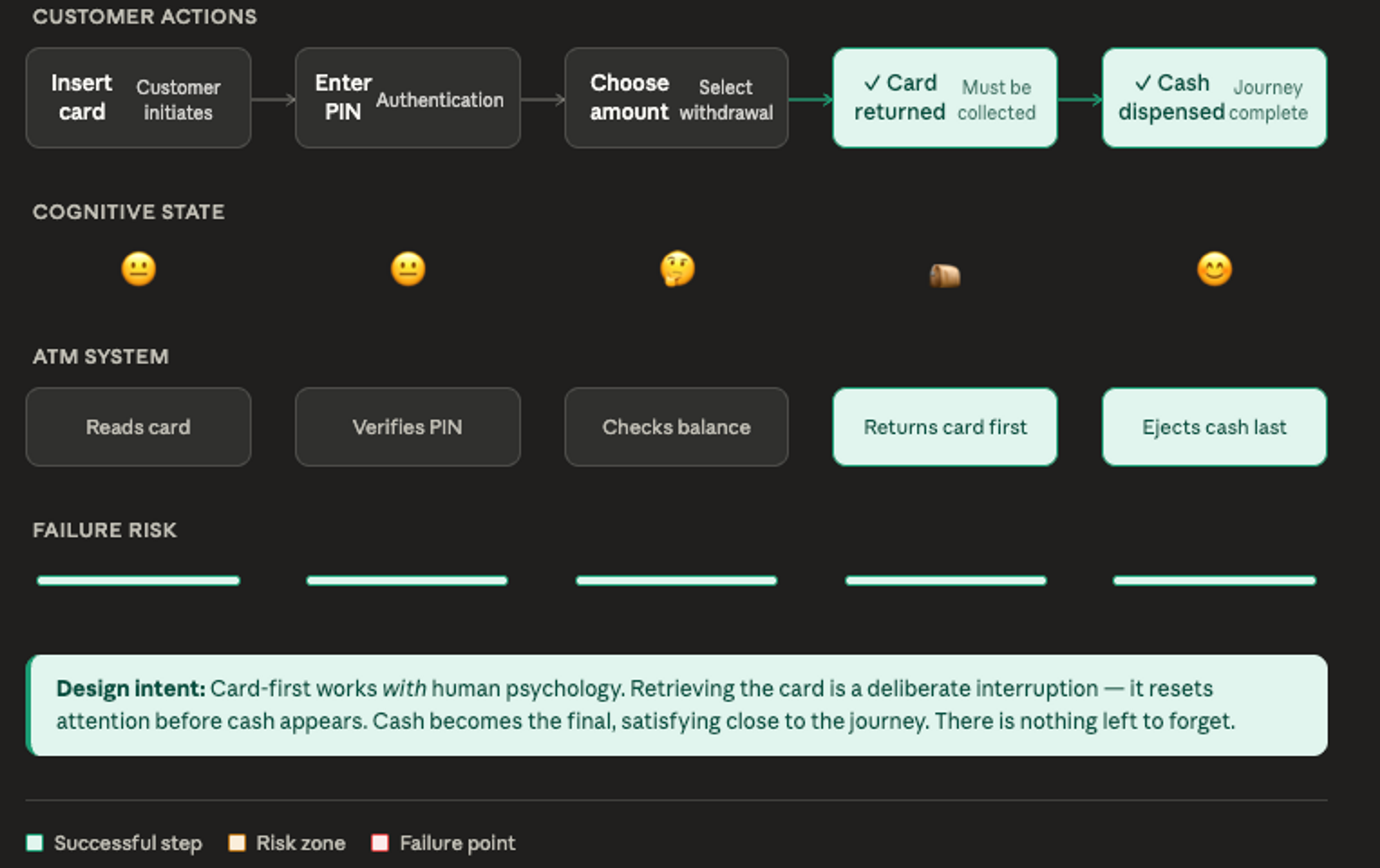

I remember withdrawing cash from an Automated Teller Machine (ATM) in the United Kingdom and pausing at a small detail: the machine returned my bank card first, and only then dispensed my cash. In Nigeria, I’m used to the reverse - cash first, card after.

When I replayed the journey, it became obvious why the order matters. Once cash is in your hand, your brain often switches into completion mode, especially if you’re in a hurry or aware of people waiting behind you. That’s exactly when it becomes easiest to forget the final step: collecting your card.

Nigeria’s “cash-first” sequence isn’t just a bank preference. The Central Bank of Nigeria (CBN) directs that cash should be dispensed before the card “to minimise the possibility of customers leaving cash uncollected at the ATM.”

This, and other guidance from CBN mandating that banks use prompts (message/voice) to reduce the likelihood of customers leaving cards behind, suggests that regulation is optimising around one failure mode: abandoned cash.

CBN’s rationale is understandable, and could be shaped by considerations like the financial literacy of the population. Dispensing the cash first reduces the failure mode of early walk-aways, and the conflict that might arise from confusion as to who abandoned cash belongs to.

Historically, UK cash machines followed the same sequence, returning the card at the end of the transaction. Later, many ATM designs moved toward returning the card before cash. Design commentary suggests this was driven by the same insight I had observed: once people have cash in hand, they are more likely to forget their card.

Nigeria is not alone in designing for abandoned cash. Argentina ATMs also operate cash-first, and the phenomenon of forgotten cards has been noted there as an avoidable problem for customers.

Both abandoned cash and abandoned cards represent potential failure modes: points in the service where the system might let down the user.

But applying service design enables you to actively consider the end-to-end user experience: the different failure modes you are designing for, and their impacts on the customer and the organisation.

While there is no publicly available data showing the volume of forgotten cards in Nigeria, we can make some rough estimates to calculate the cost they incur for the organisation and the customer.

CBN’s e-payment statistics show 1,012,277,981 ATM transactions in 2023.

At that volume, even a tiny forgotten-card rate becomes a huge number. Assuming that forgotten-card incidents happen 0.01 - 0.05% of the time, that results in somewhere between 100,000 and 500,000 incidents per year.

The cost for customers

Even apart from the burden of dealing with instances of blocked accounts or potentially fraud exposure triggered by the lost card, the cost to the customer goes beyond the fee they must pay for a replacement.

Assuming that a customer pays 1000 naira on average to get a replacement card and makes two bank visits (one to resolve/block/log the issue, and another to collect/activate a replacement), with each round trip using an okada costing 839 naira per round trip, it could cost customers up to 1.35 billion naira per year.

This is before we consider the time they must invest in that process, and the hours they are unable to spend working and earning.

The cost for organisations: service degradation

For the banks themselves, the main impact of lost cards is the opportunity cost: the time consumed by resolving cases that could be spent elsewhere.

The complexity of resolving cases depends on whether the card is lost at an ATM belonging to the user’s bank. But if we assume that each incident consumes even 10-20 minutes of combined staff handling time across call centres, branches, and back-office operations, then the system (on our 0.05% failure estimate) is diverting up to 168,713 staff-hours per year.

Taking into account the monetary value of that staff time, lost card cases could translate to a cost of 158 million naira per year for the banking sector (assuming an average salary of 150 thousand naira per month for customer service representatives).

That figure sits alongside the most significant cost, and one you can’t quantify: the opportunity cost. If staff are spending hundreds of hours every day not resolving other customer issues - failed transfers, disputes, onboarding problems, complaints, - then customers are enduring long waits to see those issues resolved, and the quality of the service degrades for everybody.

This service degradation, and its spiralling costs, illustrates the domino effect of failure demand.

For Nigeria’s banks, the example highlights an obvious limitation when it comes to service design: regulation. If the way you design your journey is dictated by external factors like CBN’s regulation and the cultural context it sits within, then your ability to design for your customers’ needs is limited.

But even with constraints and other costly failure modes to trade off against, you can use a service design approach to deliver a better service for your users by considering all the factors across an end-to-end journey that are within your control.

In this case, that’s things like timing, prompts, exception handling, and dispute processes.

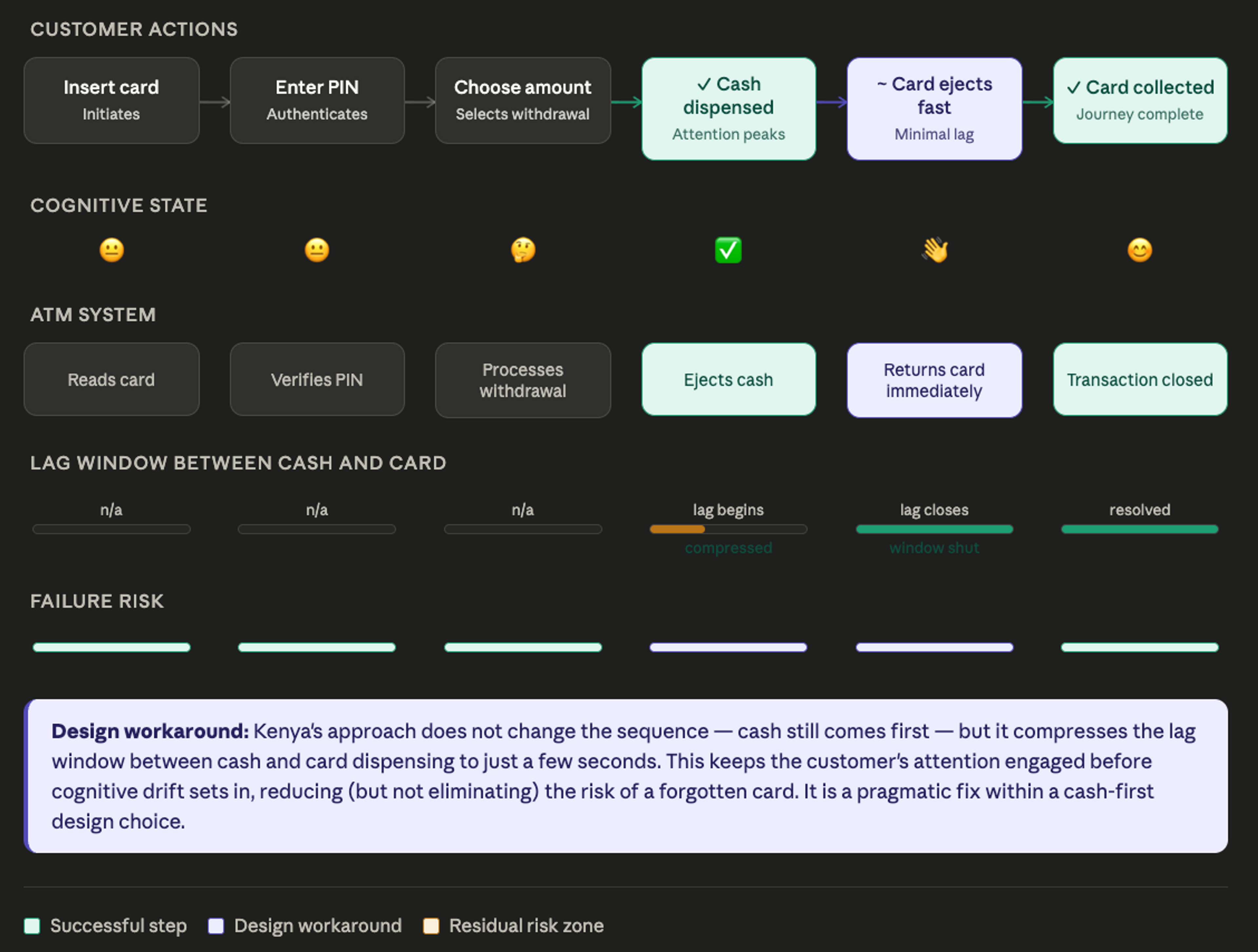

With Nigeria’s ATMs, a practical workaround lies not only in the order, but the timing. A variation I’ve noticed in some Kenya’s ATMs is the reduced “lag window” between cash and card dispensing. In these cases the card comes out almost immediately after the cash, reducing the likelihood that a customer will walk away without their card.

An approach like this gives your organisation the best chance of protecting users from predictable human mistakes, without overloading the system.

The example above focused on banking and ATMs, but the lessons are universal.

All organisations are constrained to some extent in how they deliver their services, and no organisation can expect to incur 0 costs from failure points in how customers use the service.

The organisations which incur the least - and which best manage the limits of their constraints - are the ones which have applied the techniques of service design.

Those organisations have carefully considered their end-to-end user experience; anticipating where users are most likely to slip up and redesigning the service so that the most likely mistakes are less painful - for the organisation and for its customers.

This isn’t just about the financial impact. It is about recognising where friction within your service - for both your staff and your customers - is avoidable and reducible. It is about building a culture where your users are truly at the centre of how you operate.

Principal Consultant